Crypto custody firm BitGo ($BTGO) officially rang the opening bell at the New York Stock Exchange on January 22nd, Eastern Time.

This company, seen as the "lifeline of crypto asset infrastructure," completed its IPO at $18 per share, opening at $22.43 and surging approximately 25% on its first day, firing the starting gun for the 2026 wave of crypto company listings.

Calculated at the IPO price, BitGo's valuation is approximately $2 billion. Although this figure is far below the nearly $7 billion valuation of stablecoin issuer Circle ($CRCL) which went public last year, as one of the first major crypto companies to list this year, BitGo's performance is considered steady.

Ten Years in the Making: From Multi-Sig Pioneer to Institutional Guardian

BitGo is the latest native crypto company attempting to enter the public markets, following the successful listings of several crypto firms in 2025.

Its story begins in 2013, when the crypto world was still in its "wild west" era, with frequent hacker attacks and private key management being a nightmare. Founders Mike Belshe and Ben Davenport keenly observed that if institutional investors were to enter, what they needed was not fancy trading software, but a sense of "security".

BitGo founder Mike Belshe

Standing on the podium at the NYSE, Mike Belshe might recall that afternoon over a decade ago.

As one of the first ten employees of the Google Chrome team and a foundational figure behind the modern web acceleration protocol HTTP/2, Mike was initially skeptical of cryptocurrency, even suspecting it was a scam. But he used the most "programmer" way to debunk it: "I tried to hack Bitcoin, and I failed."

This failure instantly turned him from a skeptic into a hardcore believer. To find a safer place for the old laptop full of Bitcoin under his sofa, he decided to personally dig a set of "trenches" for this wild market.

The early BitGo office was more like a laboratory. While contemporaries like Coinbase were busy acquiring users and boosting retail trading volume, Mike's team was researching the commercial potential of multi-signature (Multi-sig) technology. Despite his close personal ties with Netscape's founding bigwigs and a16z's head honcho Ben Horowitz, he did not choose the fast track of "VC acceleration," but instead took the slowest and steadiest path.

BitGo pioneered multi-signature (Multi-sig) wallet technology, which later became an industry standard. However, BitGo did not stop at selling software; it made a crucial strategic choice: to transform into a "licensed financial institution".

By obtaining trust charters in South Dakota and New York, BitGo successfully became a "qualified custodian." This status played a stabilizing role in the wave of crypto ETFs in 2024 and 2025. When asset management giants like BlackRock launched Bitcoin and Ethereum spot ETFs, it was underlying service providers like BitGo that were responsible for safeguarding the assets and handling the settlement processes.

Unlike Coinbase and other exchanges, BitGo built a solid "institutional flywheel": first, lock in assets (AUM) with极致ly compliant custody, then衍生出 (derive) staking, clearing, and prime brokerage services around these deposited assets.

This "infrastructure first" logic has given BitGo remarkable resilience amidst market volatility. After all, regardless of bull or bear markets, as long as the assets remain in the "vault," BitGo's business continues.

10x Price-to-Sales Ratio, What's the Basis?

Looking at the financial data disclosed in BitGo's prospectus, the numbers appear quite 'intimidating'.

Due to US GAAP (Generally Accepted Accounting Principles) requirements, BitGo must record the full principal of transactions as revenue. This led to a staggering "digital asset sales" gross revenue of approximately $10 billion in the first three quarters of 2025. But in the eyes of mature investors, these figures are merely "pass-through money" and do not reflect true profitability.

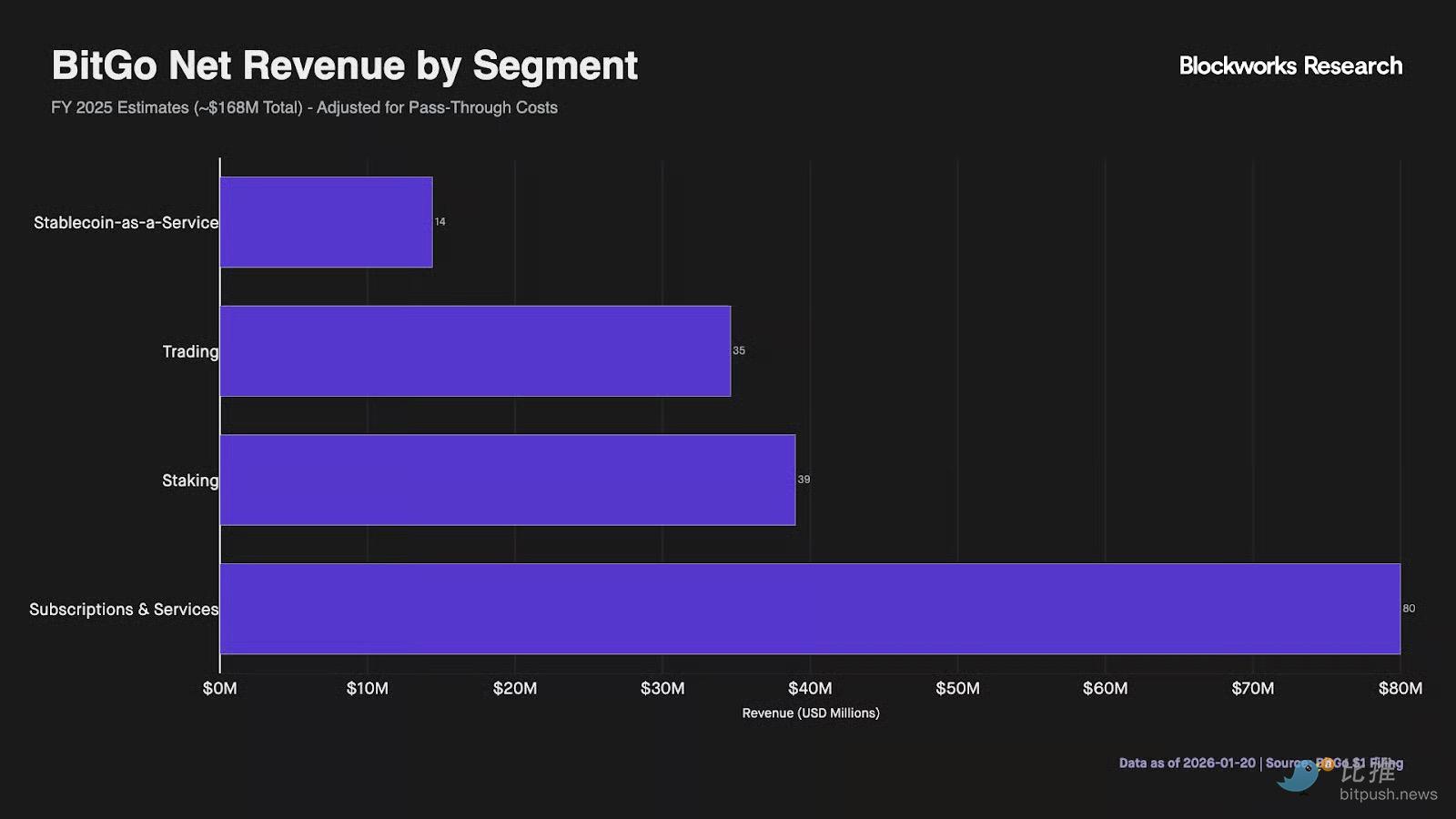

What truly supports its $2 billion valuation is the "Subscription & Services" business segment.

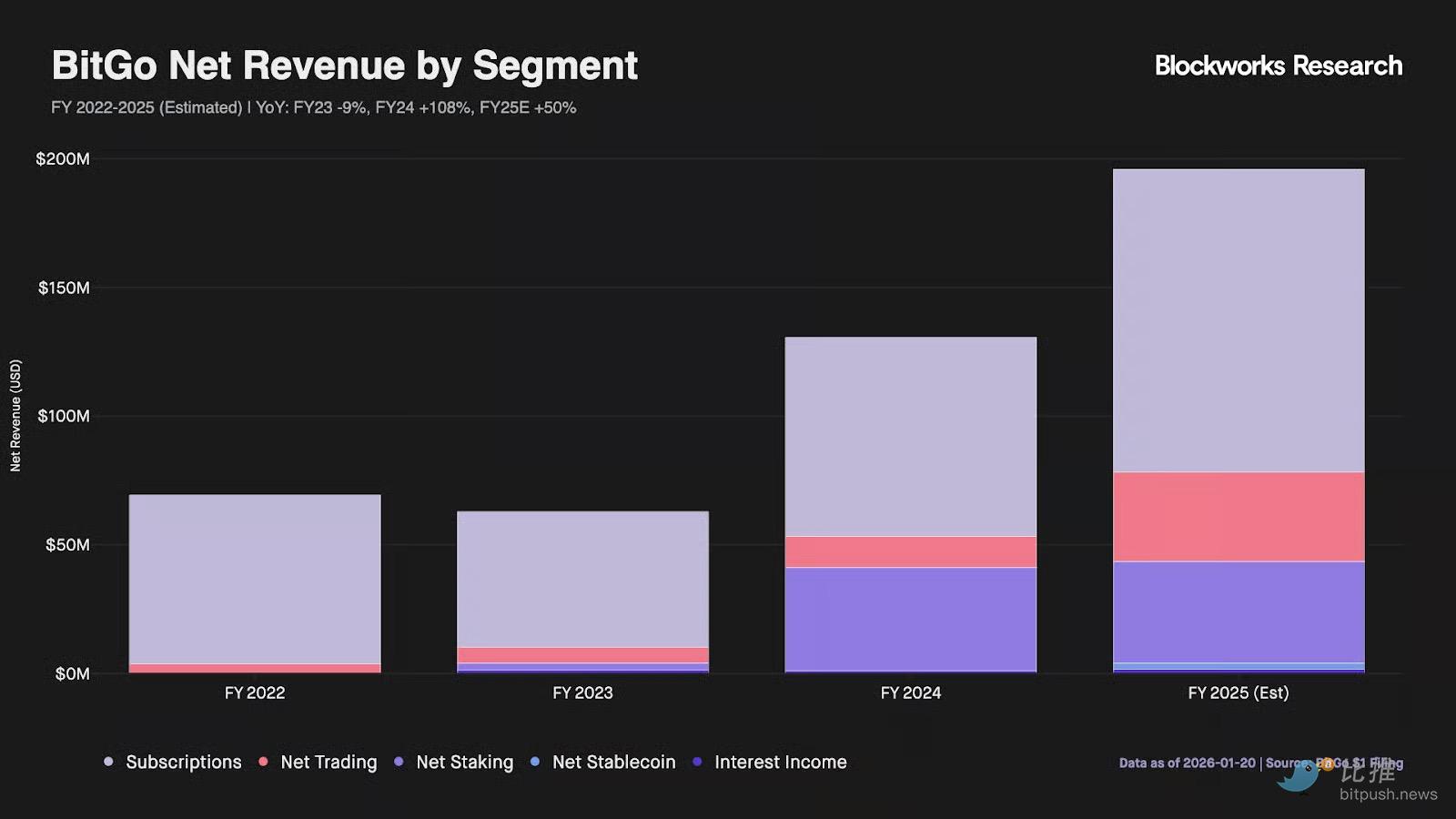

According to chart data from Blockworks Research, BitGo's core economic revenue (excluding pass-through fees and costs) is estimated to be approximately $195.9 million for the 2025 fiscal year. Subscription business contributes the vast majority of high-margin recurring revenue, with $80 million contributing nearly 48% of the total net revenue. This revenue primarily comes from recurring fees charged to over 4,900 institutional clients.

Furthermore, staking business became an unexpected growth driver. Staking revenue reached $39 million, ranking second. This reflects that BitGo is no longer just a simple "vault"; by providing value-added returns on top of custodial assets, it significantly improves capital efficiency.

Looking at the trading and stablecoin business, although trading volume accounts for the highest proportion of total revenue, it only constitutes $35 million in adjusted net revenue.

The newly launched "Stablecoin-as-a-Service" contributed $14 million. Although it's just starting, it has already demonstrated certain market penetration.

To understand BitGo's true valuation, its paper financial metrics need adjustment. If calculated based on its roughly $16 billion GAAP revenue, its valuation seems very low (P/S ratio ~0.1x). But after剔除 (removing) pass-through trading costs, staking sharing, and payments from stablecoin issuers and other non-core items, the moat of its core business is deep:

2025 Fiscal Year Core Economic Revenue (Est.): ~$195.9 million

Implied Valuation Multiple: Enterprise Value / Core Revenue ≈ 10x

This 10x valuation multiple places it above wallet-focused peers reliant on retail business. The premium部分 (partially) reflects its regulatory moat as a "qualified custodian." Simply put, at a $1.96 billion valuation level, the market is willing to pay a premium for the subscription business, with the low-margin trading and staking businesses being just the icing on the cake.

VanEck Research Director Matthew Sigel believes that BitGo's equity assets are superior to the vast majority of crypto tokens with a market cap exceeding $2 billion, as the latter have mostly never generated any net profit for their holders. BitGo's business is essentially "selling shovels." As long as institutions are trading, ETFs are running, and assets need storing, BitGo earns fees. This model might not be as flashy as some altcoins in a bull market, but in volatile and bear markets, it's an "iron rice bowl".

Stock Tokenization on IPO's First Day

Unlike other crypto company IPOs, BitGo adopted a more "crypto-native" approach: by partnering with Ondo Finance, it synchronized its shares on-chain on the very first day of listing.

The tokenized BTGO shares will circulate on Ethereum, Solana, and BNB Chain, allowing global investors to接入 (access) this newly listed custody机构几乎瞬时地 (almost instantly). Tokenized BTGO stock may in the future be used as collateral directly in DeFi lending protocols, bridging TradFi (Traditional Finance) and DeFi.

Summary

BitGo's IPO attempt continues the warming trend of the crypto equity financing market since 2025. Against the backdrop of Bitcoin spot ETF approvals and gradually clearer regulatory frameworks, institutional service providers are becoming important targets for public market investors looking to allocate crypto assets.

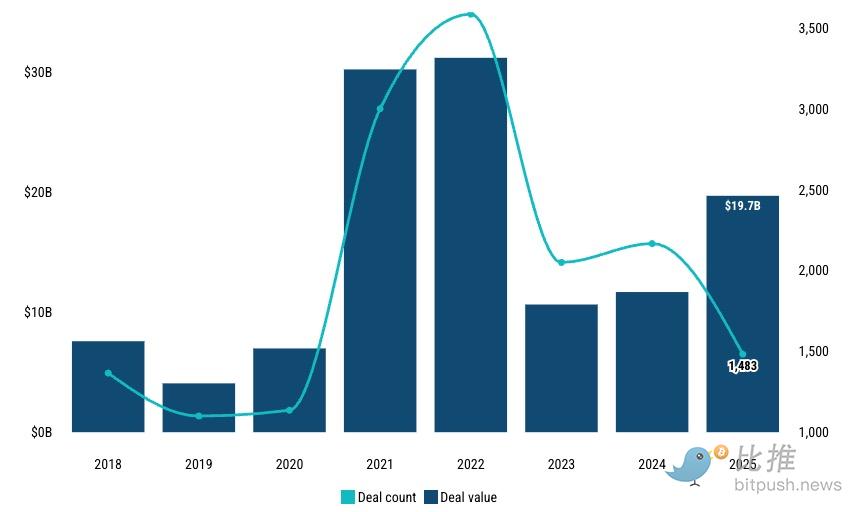

Source: PitchBook

Looking back at 2025, crypto venture capital (VC) deal value surged to $19.7 billion. As PwC IPO expert Mike Bellin stated, 2025 completed the "professionalization transformation" of cryptocurrency, and 2026 will be the year of彻底爆发 (complete) liquidity explosion.

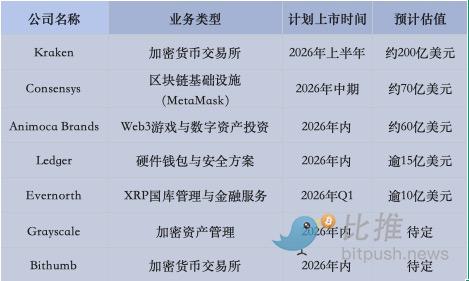

Following the successful上岸 (landing) of pioneers like Bullish, Circle, and Gemini in 2025, crypto company listings have shown dual characteristic of "infrastructuralization" and "giantization." Currently, Kraken has submitted a confidential application to the SEC, aiming for the largest crypto exchange IPO of the year; Consensys is working closely with J.P. Morgan seeking capital influence in the Ethereum ecosystem; and Ledger, amidst the wave of self-custody demand explosion, has also targeted the New York Stock Exchange.

Of course, the market has never shaken off macro fluctuations, and memories of some companies falling below their IPO price immediately after listing in 2025 are still fresh. But this恰恰说明 (precisely indicates) the industry is maturing; capital is no longer paying for every good story but is starting to scrutinize financial health, compliance frameworks, and sustainable business models.

Author: Bootly

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush